Transitioning from adolescence into adulthood ushers in the winds of amazing change: gaining new independence, getting a job, and enjoying building life solely on one's very own terms. This usually, however, comes with a less glamorous companion—that of financial responsibility. The intricate knot of the money world seems to remain daunting for most of the youngster, with student loans, mortgages, and infinite possibilities pulling in an endless number of different directions.

It is very easy to have oneself get carried away in young adulthood and forget about budgeting. In reality, the habits inculcated into practice shall be a later testimony of life. We will be covering budgeting, saving, investments, and managing costs, along with the physiology of spending. Let's face it: the way to success is not only through numbers but also through your intuition and behavior.

So, let the financial journey begin now. After all, it's never too early or too late for a brighter and better financial future.

Take control of your finances today!

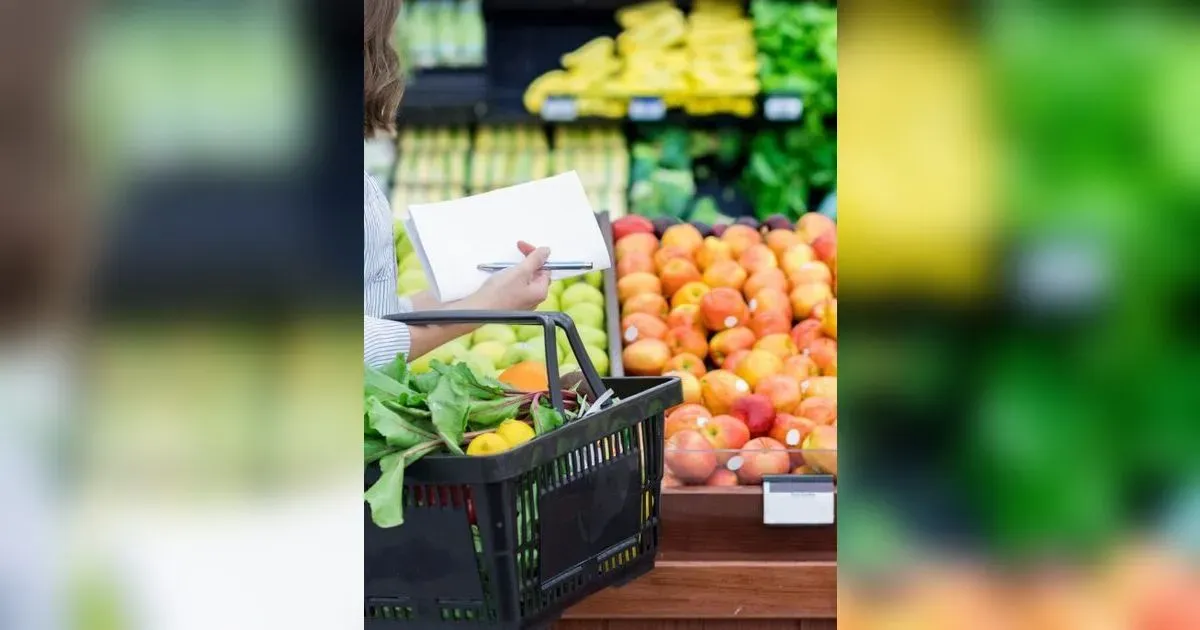

1. Make a budget and stick to it: Financial cornerstones for young people

- understanding the importance of budgeting

Budgeting tends to bring organization and simplification throughout one's life. Budgets will help indicate where the money is being spent and therefore important when the money is channeled to your needs, wants, and saving goals. Most of the time, a budget is always an important tool to use for most young people with responsibilities involving education, starting a new career, and building one's independence.

- Why budgeting is important for young adults

✓Financial management: This section is taken care of by financial management, which, through the acquisition of such skills, enables the youths to be able to manage their finances without losing their grip on the money that slips through their fingers.

✓ Goals: Be it to save towards a house deposit, a financing for the holiday of a lifetime, or aspiring to gain an education, it requires you to have goals in order to have an avenue for the cash flow to tour through and vice versa.

✓Debt Management: With the youths probing into those linked and outbound, they could, in turn, trace paths by which the budget can be whittled down, thus reducing expenses and creating provisions for an emergency fund.

✓Develop good habits: Financial habits generated in early life that are indeed the most powerful tools in the long run in their financial stride.

✓ Goals: Be it to save towards a house deposit, a financing for the holiday of a lifetime, or aspiring to gain an education, it requires you to have goals in order to have an avenue for the cash flow to tour through and vice versa.

✓Debt Management: With the youths probing into those linked and outbound, they could, in turn, trace paths by which the budget can be whittled down, thus reducing expenses and creating provisions for an emergency fund.

✓Develop good habits: Financial habits generated in early life that are indeed the most powerful tools in the long run in their financial stride.

- Creating an effective budget

• Track all sources of income, be it wages, part-time job, or financial aid.

• Categorize all expenses: Fixed can take the form of rent, utilities, and any variable ones, such as for sales and entertainment.

• Allocate revenue into different groups basing on priorities and goals.

• Review: Regularly look over your expenses and reallocate budgets if required. Do not Overspend

• Be Realistic: Never put a budget limit which is too difficult to follow.

• Use Budget Tools: It can be easily tracked with apps or spreadsheets

• Automate Savings: Have opened savings accounts

• Reward yourself: For every financial milestone that you reach, buy yourself some reward so that you stay motivated

• Flexibility: Be aware of the fact that there comes the unexpected expenses. Adjust the budget End.

Young adults have several possible ways they could employ to reach their financial well-being, such as drawing and holding onto an effective financial plan. This tool aids in viewing the incomes versus the expenses and in effect, helps make proper decisions towards any set goal. Having learned early in life how to manage finances properly, a young adult paves the way toward building a great future and solid financial foundation.

• Categorize all expenses: Fixed can take the form of rent, utilities, and any variable ones, such as for sales and entertainment.

• Allocate revenue into different groups basing on priorities and goals.

• Review: Regularly look over your expenses and reallocate budgets if required. Do not Overspend

• Be Realistic: Never put a budget limit which is too difficult to follow.

• Use Budget Tools: It can be easily tracked with apps or spreadsheets

• Automate Savings: Have opened savings accounts

• Reward yourself: For every financial milestone that you reach, buy yourself some reward so that you stay motivated

• Flexibility: Be aware of the fact that there comes the unexpected expenses. Adjust the budget End.

Young adults have several possible ways they could employ to reach their financial well-being, such as drawing and holding onto an effective financial plan. This tool aids in viewing the incomes versus the expenses and in effect, helps make proper decisions towards any set goal. Having learned early in life how to manage finances properly, a young adult paves the way toward building a great future and solid financial foundation.

2. Start saving early: The cornerstone of financial health for young adults

One of the core rules in one's financial life is saving. There are so many long-term dividends that result when one starts saving at an early age.

- The power of compounded interest

✓Time is your friend: The more time you can spare for having started an investment, the more time you will have for growing the money.

✓ Magic of Compounding: Return on the first investment also earns interest, which builds up and snowballs into a huge amount.

✓Long-Term Savings: Large amounts of money saved consistently over many years has the potential to result in large accumulation

✓ Magic of Compounding: Return on the first investment also earns interest, which builds up and snowballs into a huge amount.

✓Long-Term Savings: Large amounts of money saved consistently over many years has the potential to result in large accumulation

- Creating a Safety Net

•Emergency Savings: This wipes out financial stress by saving money from unpredictable expenses like medical bills or car repairs.

• Reducing your dependence on credit: If you have a savings account, you will have no urge for high-interest loans.

•Peace of Mind: knowing you have someone to help you can reduce future anxiety.

• Reducing your dependence on credit: If you have a savings account, you will have no urge for high-interest loans.

•Peace of Mind: knowing you have someone to help you can reduce future anxiety.

- Achieving major goals in Life

•House: Since you have saved for a long period of time, you can pay a larger initial deposit.

• Education: Saved accounts can grow into bigger amounts to finance higher education or other vocational courses quickly.

• Retirement: Preparing retirement accounts at an early age can get you much more balance in the future.

• Education: Saved accounts can grow into bigger amounts to finance higher education or other vocational courses quickly.

• Retirement: Preparing retirement accounts at an early age can get you much more balance in the future.

- Principles on the Wise Handling of Money

• Discipline: In regular saving, you practice some financial discipline on yourself.

• Planning for the future: Big savings will have you think hard on the long term.

• Reduces the cost of emergency spending: Appropriating budgeting will help cut emergency spending.

In other words, saving early is like sowing a seed for your fiscal future. Thus, it can turn out to be a prolific investment garden with complete care and timely watering.

Learning how to value accumulated profits and building a safety net while working leads to realizing a long-term goal, which can be the way a young adult sets up for financial success.

• Planning for the future: Big savings will have you think hard on the long term.

• Reduces the cost of emergency spending: Appropriating budgeting will help cut emergency spending.

In other words, saving early is like sowing a seed for your fiscal future. Thus, it can turn out to be a prolific investment garden with complete care and timely watering.

Learning how to value accumulated profits and building a safety net while working leads to realizing a long-term goal, which can be the way a young adult sets up for financial success.

3. Understanding building credit: financial tip for young adults

Building credit are the ambulance and gauze of young people's money health. It's like establishing a base to build the house; with a fine credit score, one is enabled to make better investment opportunities in the years to come.

- What then is credit?

A credit is where one is given an advance that you can later agree to fully repay. It is, therefore, a system through which one can obtain and pay for goods or service over a more extended period.

- Why is it important for young people?

✓Leasing: Most landlords check your credit score to be able to lease to you.

✓Buying a car: Better credit leads to better car loan interest. rates

✓Borrowing: A strong credit history is mandatory for borrowing a home loan.

✓Job: There is a possibility that an employer's may look at your credit card.

✓Cheap-Interest rates: Good credit history leads to cheap interest rates on loans and credit cards.

- How to build credit

•Start early: The sooner you start building your credit, the better.

• Use credits card wisely: This means making payments on time, not letting credit card debts pile up, and holding such debts to the minimum level possible.

• Always check your credit report for errors and omissions.

• Avail yourself of secure credit cards; these will help you clean up the setbacks in setting up your credit history fast.

• Pay off your debt : First settle the high-interest debt.

•Apply a mix of your spending toward your debt:Credit cards, Loans, may help.

Through understanding how credit works, then actively building an awesome credit history, young adults can prepare themselves to find success through finance. In other words, one will earn the trust of the lenders by undertaking proper practices of finance. Besides, issuing out loans is a slow process; hence the need to exercise patience and steadiness.

• Use credits card wisely: This means making payments on time, not letting credit card debts pile up, and holding such debts to the minimum level possible.

• Always check your credit report for errors and omissions.

• Avail yourself of secure credit cards; these will help you clean up the setbacks in setting up your credit history fast.

• Pay off your debt : First settle the high-interest debt.

•Apply a mix of your spending toward your debt:Credit cards, Loans, may help.

Through understanding how credit works, then actively building an awesome credit history, young adults can prepare themselves to find success through finance. In other words, one will earn the trust of the lenders by undertaking proper practices of finance. Besides, issuing out loans is a slow process; hence the need to exercise patience and steadiness.

4. Educate yourself about investing: financial advice for young adults

Educating yourself about is learning how you can make your money work for you. It's an understanding of the financial vehicles, how they work, associated risks, and potential pitfalls that could be a result of them.

- Why Young People Should educate themselves

✓Time is on your side: As a dependent young adult, being time-rich is a huge advantage. The magic of compounding coupled with accumulated profits will be true even with a small and periodic investment done for a handful of years on various occasions.

✓Wealth Creation: Power of investing is always going to reside in chiseling out huge corpus, in the long run, without much fuss. This is the very base of financial independence.

✓Risk reduction: Knowledge is power. Knowledge of investing makes you make informed decisions, and hence the chance to lose money is very minimal.

✓Goal Achievement: Saving enables one to accomplish some set financial goals that an individual sets like a home or business settlement and retirement.

- How does it start up?

✓Basic finance skills: This involves the knowledge of basic finance concepts applicable in a normal home or business situation such as budgeting, saving, and managing costs.

✓Funding Basics: Describe the various types of investment that exist such as stocks, bonds, mutual funds, ETFs and real estate and how they actually work in practicality

✓Risk Tolerance: what amount of risk do you feel comfortable taking, and what types of investments are going to lead to the best results for you?

✓Start small: Begin small but invest regularly to create an impact of compounding returns.

✓Seek knowledge: Gain more knowledge by using the Internet, books, and financial advisors.

In essence, it will basically afford financial right to the youth to make an informed choice on finances, facilitate wealth accumulation, and even ensuring a better financial future in terms of a better laid foundation. It is so proactive; you get to have control over your financial destiny.

5. Limit debt: financial tip for the young adult

Debt could be a double-edged sword for the youth. Although it fulfills the multiple starting-up business or education expenses, at the end of the day, most likely it would cause long-term financial burden if not properly managed.

- Why would debt limitation is important

✓Interest rates: Most loans are usually charged an interest rate, which can multiply the overall cost of the purchase. The longer the period of the loan, the more interest would mount.

✓Economic reforms: Excessive debt levels can bind economic freedom. One cannot save, invest, or buy large items for emergencies.

✓Less stress: Crushing debt includes a lot of money stress. And this stress can carry over into your mind and emotions.

✓Borrowing: Smart usage of credit cards can also help you build your credit. Although too much debt will negatively impact your credit score.

- Cost control

✓ Budget: A good budget is something that is created to track one's income and expenses properly. One would clearly see areas in which you can cut back and apply income on paying the debt.

✓ Debt pay priority: First of all, make a plan to repay your debts and put high-interest debts on top priority. One should think about emergency debts, or someone should use snowboarding strategies.

✓Refrain from impulse buying: Keep asking oneself before one indulges: "Is it a need or just a desire?" and thus avoids impulse buying for the heck of avoiding instant buying.

✓Build an emergency account: To avoid using immediate credit as an option to cope with emergent expenses, one should benefit from saving for an unexpected expenses account.

✓Educate on personal finance: Learn on personal finance and spending. This will help in making conscious choices and remain in control of the finances.

Reduction of debt is one side of the class factor of the youth's financial viability. Making conscious choices and establishing good financial habits will help in laying down sound financial paths and help in the achievement of the long-term objectives. Remember, there is no perfect time to service your debts and become financially independent.

Conclusion

It truly is a blur of time, experiences, probing at careers, and freedom. But yet in the middle of this new excitement, there is one thing absolutely to be gripped tightly: your financial foundation. By following these tips, you are not saving; you are investing in your future. Remember, the traveling toward financial literacy is a journey, not a destination. It is about growing, not perfection. With small but consistent moves come the tremendous long-term outcomes.

Never fear approaching financial advisors. Their advice offers a way of thinking. More importantly, it makes an individual have a positive relationship with money. Understand the possibilities, respect its shortcomings and use them to get to your dreams.

The challenge is that investments you make now pay off for the future. Starting out early does the trick and definitely assures the chance of a lifetime for long-term financial security and opportunity. Rise to the occasion; learn, make adjustments, and grow. Your future self will surely thank you.

Experiment, determine what is truly important, what correlates to your goals, and what fits into your life. The key is to start now and continue. Your financial well-being is in your hands.

Never fear approaching financial advisors. Their advice offers a way of thinking. More importantly, it makes an individual have a positive relationship with money. Understand the possibilities, respect its shortcomings and use them to get to your dreams.

The challenge is that investments you make now pay off for the future. Starting out early does the trick and definitely assures the chance of a lifetime for long-term financial security and opportunity. Rise to the occasion; learn, make adjustments, and grow. Your future self will surely thank you.

Experiment, determine what is truly important, what correlates to your goals, and what fits into your life. The key is to start now and continue. Your financial well-being is in your hands.

{kind=link}